In a time when generational change is upon us, it has never been more important to be ahead of the pack.

Thinking creatively and providing flexibility is crucial in delivering financial services that meet the needs of the emerging generations. Consider that by 2025, Gen Alpha (born after 2010) will be the largest generation in history.

One in two will obtain a university degree and they are expected to have 18 jobs over six careers in their lifetime.

However, only 29% of grandparents currently provide any financial support for their grandchildren’s education.

We know that baby boomers are spending up, treating themselves to holidays and personal discretionary items. However, younger generations are tightening their purse strings due to cost-of-living pressures and rising interest rates.

While these different generations are currently in vastly different situations, the tides will shift over the next few decades as the biggest wealth transfer in history starts to play out.

So, what can you as a financial adviser do to address the changing tide?

It’s timely to consider how the financial strategies you are recommending today will solve for both the ageing and emerging generations.

To do this, flexibility in product design and strategies will be essential.

Scenarios will need to be meticulously laid out, and the products used to solve them will need to be considered and agile.

What’s the answer to addressing generational change in financial advice?

Meet Joe and Jill.

Joe and Jill are 76 and financially comfortable. They are Boomers! They still reside in their family home, have a seaside investment property, share portfolio and cash through their family trust.

They live a comfortable life but are concerned by the possible introduction of changes to the tax on high superannuation balances.

Jill still draws a wage from directors fees. They have a few concerns about the future, most notably potential health issues they may face and the resultant need for medical assistance.

They also worry about the financial wellbeing of their children and grandchildren. They aspire for their grandchildren to have a quality education, and to help them with a first home deposit.

They are aware that carrying any debt from education can be a lifelong burden with the average HECS/HELP balance currently sitting at $22,636.

These days just those two aspirations can set young people back more than $200,000. Joe and Jill have already set aside $500,000 for their grandchildren and plan to contribute further funds as they gradually sell down other assets.

They are seeking the assistance of a financial adviser to set up a structure to meet their needs and ensure their hard-earned savings go to their loved ones.

A solution

While there are several established products that can be used to build and transfer wealth in a tax effective way, a more recent player in the market deserving of attention is the modern iteration of the education bond.

These bonds offer a blend of tax advantages, flexible investment strategies, and wealth transfer capabilities that set them apart.

Designed to tackle the mounting costs of education, these bonds offer flexibility rarely found elsewhere.

Not only can they accumulate funds for education expenses (think school fees, computers, textbooks, school trips etc) but they also provide the freedom to withdraw capital for non-education needs at any time without triggering any tax events.

Back to Joe and Jill...

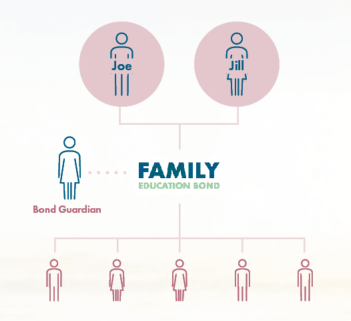

Joe and Jill’s financial adviser recommends a Family Education Bond be set up with the following structure:

Why an Education Bond?

- This flexible structure allows for the tax-free withdrawal of capital at any time, for any purpose. So, if Joe and Jill need funds for any unforeseen expenses, they can access their investment at any time. This feature also solves Joe and Jill’s longevity risk concerns.

- The ability to appoint multiple beneficiaries means Joe and Jill can nominate all five of their Grandchildren as beneficiaries, with any future grandchildren able to be added at any stage.

- Education bonds are tax-paid investments, so Joe and Jill don’t have to be concerned with tax reporting and paying tax (or CGT) on ongoing fund earnings. Tax is paid at a maximum rate of 30% (often much lower) within the fund by Futurity, meaning it’s a tax-effective investment for Jill who is still on a high MTR.

- Valuable Education Tax Benefit that returns the 30% tax paid in the fund to the education bond’s earning component when funds are withdrawn to meet education expenses.

- By appointing their daughters as bond guardians, Joe and Jill ensure the bond continues providing for their grandchildren if they pass away, granting peace of mind that their legacy will endure.

Alternatively, with some changes to the above structure, Joe and Jill could take advantage of other estate planning features such as future dated bond transfers and ‘Will-like’ nomination features.

So, this one bond allows Joe and Jill to meet their education funding objectives for their grandchildren tax effectively, as well as helping with a future house deposit.

Most education bonds offer an extensive menu of professionally managed investment options, as well as the ability to be used as a tax-effective ‘family trust’ without the compliance costs associated with traditional trust structures. One bond, endless possibilities.

Disclaimer The information in this article contains general advice only and does not take into account your objectives, financial situation or needs. Before you act on any advice in this website please consider whether it is appropriate to your personal circumstances. You should also read the relevant Product Disclosure Statement and download the Application Form which are both available on our website, or you can obtain a copy by calling us on 1300 345 456.